August Survey Results at a Glance:

- The overall index climbed for month, but remained below growth neutral.

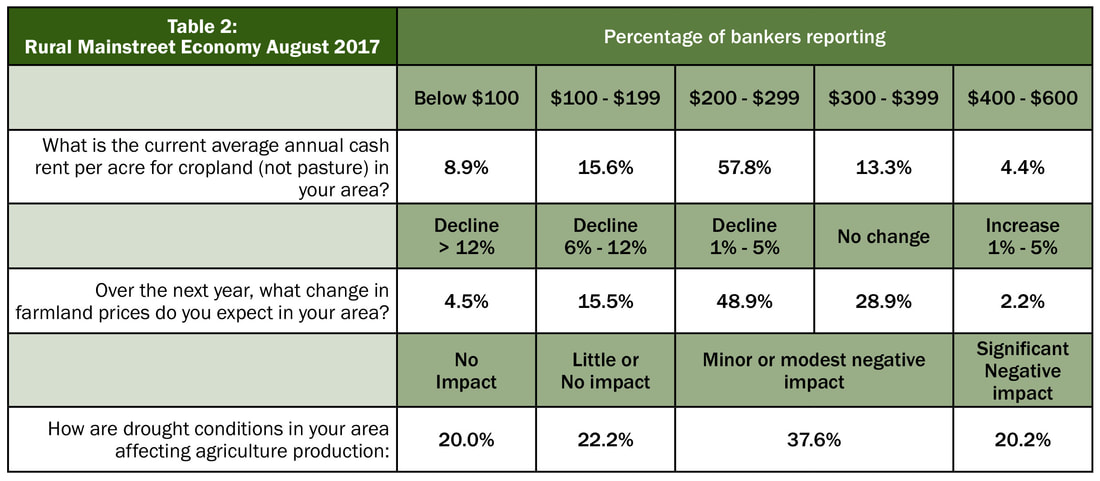

- Approximately 57.6 percent of bankers reported drought conditions were having a negative impact on agriculture production in their area,

- Average yearly cash rents declined by 4.3 percent over the past year to $241 per acre.

- On average bankers expect farmland prices to decline by another 3.5 percent over the next year. In August 2016, bank CEOs projected a 6.9 percent decline for next year.

OMAHA, Neb. (Aug. 17, 2017) – After plummeting in July, the Creighton University Rural Mainstreet Index increased slightly for August, but remained below the 50.0 threshold according to the latest monthly survey of bank CEOs in rural areas of a 10-state region dependent on agriculture and/or energy.

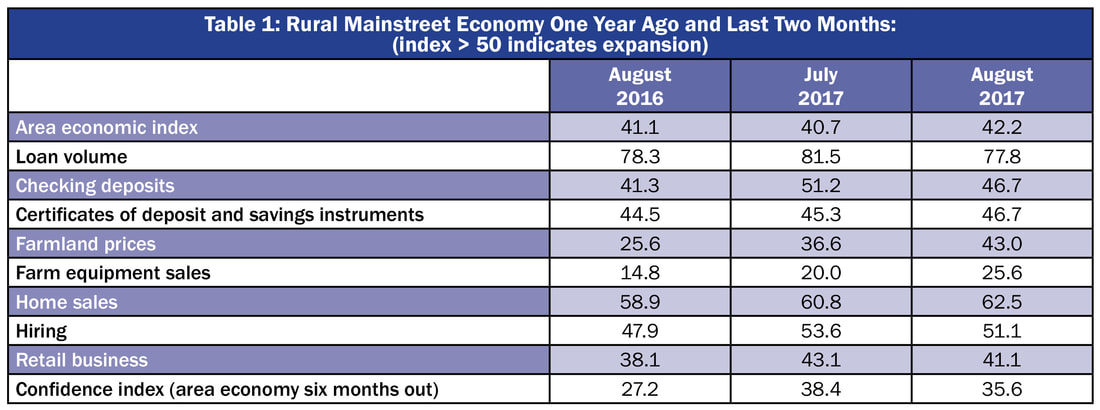

Overall: The index, which ranges between 0 and 100, increased to a weak. 42.2 from 40.7 in July which was the index’s lowest level since November of last year.

“We continue to record economic weakness stemming from low agriculture commodity prices and fallout from the drought in parts of the region. Approximately 57.6 percent of bankers reported drought conditions were having a negative impact on agriculture production in their area, “said Ernie Goss, Jack A. MacAllister Chair in Regional Economics at Creighton University's Heider College of Business.

However there was significant variability regarding the impact of weather conditions. Bryan Grove, president of American State Bank in. Grygla, Minnesota, said, “Crop conditions overall in northwest Minnesota are good. Small grain harvest is just starting, with good results both in quality and quantity.”

Overall: The index, which ranges between 0 and 100, increased to a weak. 42.2 from 40.7 in July which was the index’s lowest level since November of last year.

“We continue to record economic weakness stemming from low agriculture commodity prices and fallout from the drought in parts of the region. Approximately 57.6 percent of bankers reported drought conditions were having a negative impact on agriculture production in their area, “said Ernie Goss, Jack A. MacAllister Chair in Regional Economics at Creighton University's Heider College of Business.

However there was significant variability regarding the impact of weather conditions. Bryan Grove, president of American State Bank in. Grygla, Minnesota, said, “Crop conditions overall in northwest Minnesota are good. Small grain harvest is just starting, with good results both in quality and quantity.”

Farming and Ranching: The farmland and ranchland-price index for August rose to 43.0, its highest level since July 2014 and up from last month’s 36.6. This is the 45th straight month the index has fallen below growth neutral 50.0.

This month, and in August 2016, bank CEOs were asked the value of cash rents for cropland (not pasture) in their area. On average bankers reported a yearly cash rent of $241 per acre, which is down from 12 months earlier when bankers indicated $252 per acre. This represents a decline in yearly per acre cash rents of 4.3 percent over the past year.

On average bankers expect farmland prices to decline by another 3.5 percent over the next year. This is an improvement from this time last year when bank CEOs, on average, projected a 6.9 percent decline.

The August farm equipment-sales index increased to 25.6 from 20.0 in July. This marks the 48th consecutive month the reading has remained below growth neutral 50.0.

Banking: Borrowing by farmers was strong for August as the loan-volume index fell to a still robust 77.8 from 81.5 in August. The checking-deposit index was 46.7, down from July’s 51.2, while the index for certificates of deposit and other savings instruments increased to 46.8 from 45.3 in July.

Hiring: The job gauge dropped to 51.1 from July’s 53.6 and June’s healthy 58.9. Rural Mainstreet businesses, not linked to agriculture, increased hiring for the month, but at a slower pace than in July.

Confidence: The confidence index, which reflects expectations for the economy six months out, slumped to a weak 35.6 from 38.4 in July, indicating a continued pessimistic outlook among bankers. “Concerns about trade combined with drought conditions in portions of the region sank bankers’ economic outlook,” said Goss.

Home and Retail Sales: Home sales moved higher for the Rural Mainstreet economy for August. The August reading rose to 62.5 from July’s 60.8. The August retail-sales index sank to 41.1 from 43.1 in July. “Much like their urban counterparts, Rural Mainstreet retailers are experiencing significant pullbacks in sales,” reported Goss.

This month, and in August 2016, bank CEOs were asked the value of cash rents for cropland (not pasture) in their area. On average bankers reported a yearly cash rent of $241 per acre, which is down from 12 months earlier when bankers indicated $252 per acre. This represents a decline in yearly per acre cash rents of 4.3 percent over the past year.

On average bankers expect farmland prices to decline by another 3.5 percent over the next year. This is an improvement from this time last year when bank CEOs, on average, projected a 6.9 percent decline.

The August farm equipment-sales index increased to 25.6 from 20.0 in July. This marks the 48th consecutive month the reading has remained below growth neutral 50.0.

Banking: Borrowing by farmers was strong for August as the loan-volume index fell to a still robust 77.8 from 81.5 in August. The checking-deposit index was 46.7, down from July’s 51.2, while the index for certificates of deposit and other savings instruments increased to 46.8 from 45.3 in July.

Hiring: The job gauge dropped to 51.1 from July’s 53.6 and June’s healthy 58.9. Rural Mainstreet businesses, not linked to agriculture, increased hiring for the month, but at a slower pace than in July.

Confidence: The confidence index, which reflects expectations for the economy six months out, slumped to a weak 35.6 from 38.4 in July, indicating a continued pessimistic outlook among bankers. “Concerns about trade combined with drought conditions in portions of the region sank bankers’ economic outlook,” said Goss.

Home and Retail Sales: Home sales moved higher for the Rural Mainstreet economy for August. The August reading rose to 62.5 from July’s 60.8. The August retail-sales index sank to 41.1 from 43.1 in July. “Much like their urban counterparts, Rural Mainstreet retailers are experiencing significant pullbacks in sales,” reported Goss.

Each month, community bank presidents and CEOs in nonurban agriculturally and energy-dependent portions of a 10-state area are surveyed regarding current economic conditions in their communities and their projected economic outlooks six months down the road. Bankers from Colorado, Illinois, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, South Dakota and Wyoming are included. The survey is supported by a grant from Security State Bank in Ansley, Nebraska.

This survey represents an early snapshot of the economy of rural agriculturally and energy-dependent portions of the nation. The Rural Mainstreet Index (RMI) is a unique index covering 10 regional states, focusing on approximately 200 rural communities with an average population of 1,300. It gives the most current real-time analysis of the rural economy. Goss and Bill McQuillan, former chairman of the Independent Community Banks of America, created the monthly economic survey in 2005.

This survey represents an early snapshot of the economy of rural agriculturally and energy-dependent portions of the nation. The Rural Mainstreet Index (RMI) is a unique index covering 10 regional states, focusing on approximately 200 rural communities with an average population of 1,300. It gives the most current real-time analysis of the rural economy. Goss and Bill McQuillan, former chairman of the Independent Community Banks of America, created the monthly economic survey in 2005.

| Colorado: Colorado’s August Rural Mainstreet Index (RMI) rose to 41.8 from 39.1 in July. The farmland and ranchland-price index expanded to 42.8 from July’s 35.5. Colorado’s hiring index for August climbed to 50.4 from July’s 49.2. Illinois: The August RMI for Illinois inched up to 41.2 from 40.2 in July. The farmland-price index increased to 42.3 from July’s 36.3. The state’s new-hiring index dropped to 47.5 from last month’s 54.2. Iowa: The August RMI for Iowa expanded to 42.3 from 41.7 in July. Iowa’s farmland-price index for August advanced to a weak 43.1 from 37.3 in July. Iowa’s new-hiring index fell to 52.5 from July’s healthy 60.7. Kansas: The Kansas RMI for August climbed to 40.2 from July’s 39.4. The state’s farmland-price index grew to 41.6 from 35.8 in July. The new-hiring index for Kansas slumped to 43.0 from 50.6 in July. Minnesota: The August RMI for Minnesota slipped to 42.4 from July’s 42.8. Minnesota’s farmland-price index increased to 43.2 from 38.0 in July. The new-hiring index for the state declined to 53.1 from July’s strong 65.5. Pete Haddeland, CEO of the First National Bank in Mahnomen, reported that, ”Our crops in this area look good. Very little impact from drought. The wheat is excellent.” | Missouri: The August RMI for Missouri rose to 42.5 from 42.2 in July. The farmland-price index improved to 43.2 from July’s 42.3. Missouri’s new-hiring index declined to 53.4 from 62.8 in July. Nebraska: The Nebraska RMI for August inched forward to 42.9 from July’s 42.1. The state’s farmland-price index expanded to 43.5 from last month’s 37.5. Nebraska’s new-hiring index stood at a solid 55.2, but down from 62.5 in July. North Dakota: The North Dakota RMI for August rose to a regional high of 50.1 and up from July’s 41.5. The state’s farmland-price index moved to 44.1 from July’s 41.0. North Dakota’s new-hiring index dipped to 59.1 from 59.9 in July. South Dakota: The August RMI for South Dakota fell to 38.5 from July’s 38.9. The farmland-price index increased to 41.7 from July’s 35.4. South Dakota's new-hiring index sank to 43.4 from July’s 48.1. Wyoming: The August RMI for Wyoming rose to 41.2 from July’s 40.1. The August farmland and ranchland-price index increased to 42.3 from July’s 36.1. Wyoming’s new-hiring index slumped to 47.5 from July’s much stronger 53.0. |

Tables 1 and 2 summarize the survey findings.

(Click each table to view larger.)

(Click each table to view larger.)

Follow Ernie Goss on Twitter: www.twitter.com/erniegoss

For historical data and forecasts, visit our website: https://www.creighton.edu/economicoutlook/

For ongoing commentary on recent economic developments, visit our blog at: http://www.economictrends.blogspot.com

For historical data and forecasts, visit our website: https://www.creighton.edu/economicoutlook/

For ongoing commentary on recent economic developments, visit our blog at: http://www.economictrends.blogspot.com

RSS Feed

RSS Feed