October Survey Results at a Glance:

OMAHA, Neb.(Oct. 20, 2016) – The Creighton University Rural Mainstreet Index sank for October and remained below growth neutral for the 14th straight month, according to the monthly survey of bank CEOs in rural areas of a 10-state region dependent on agriculture and/or energy.

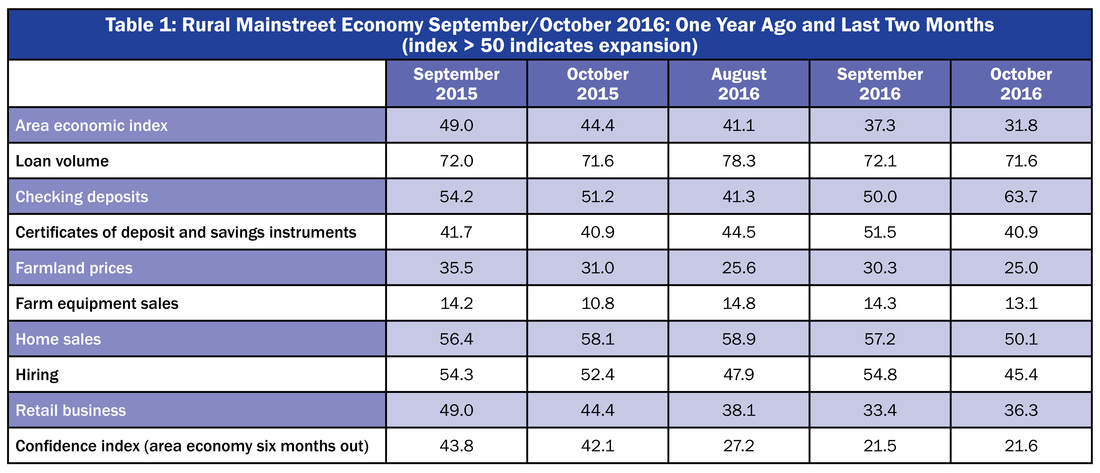

Overall: The index, which ranges between 0 and 100 fell to 31.8 from September’s 37.3. This month’s reading is the lowest recorded since April 2009.

“Over the past 12 months, livestock commodity prices have tumbled by 19.7 percent and grain commodity prices have slumped by 18.5 percent. The economic fallout from this price weakness continues to push growth into negative territory for six of ten states in the region,” said Ernie Goss, Jack A. MacAllister Chair in Regional Economics at Creighton University's Heider College of Business.

Jon Schmaderer, president of Tri-County Bank in Stuart, Nebraska said, “The calf market has now officially followed suit with grain and other livestock pricing declines.” Another bank CEO reported calf prices are going to be down 30 to 40 percent, which will have a large downward economic impact.

- For a 14th straight month, the Rural Mainstreet Index fell below growth neutral.

- Overall index slumps to lowest level since April 2009.

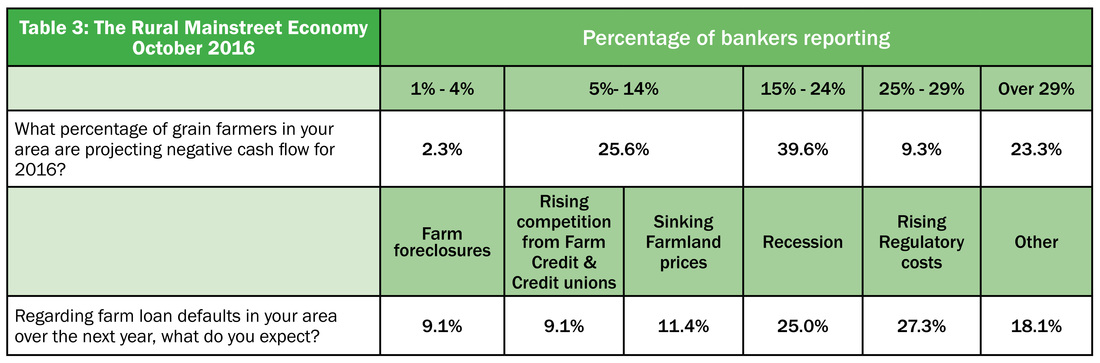

- Bank CEOs project more than one in five farmers with negative 2016 cash flows.

- More than one in four bank CEOs expect rising regulatory costs to be the biggest challenge to their bank operations over the next 5 years.

- Gains reported for Colorado, Iowa, Nebraska and South Dakota while losses were recorded for Illinois, Kansas, Minnesota, Missouri, North Dakota and Wyoming.

OMAHA, Neb.(Oct. 20, 2016) – The Creighton University Rural Mainstreet Index sank for October and remained below growth neutral for the 14th straight month, according to the monthly survey of bank CEOs in rural areas of a 10-state region dependent on agriculture and/or energy.

Overall: The index, which ranges between 0 and 100 fell to 31.8 from September’s 37.3. This month’s reading is the lowest recorded since April 2009.

“Over the past 12 months, livestock commodity prices have tumbled by 19.7 percent and grain commodity prices have slumped by 18.5 percent. The economic fallout from this price weakness continues to push growth into negative territory for six of ten states in the region,” said Ernie Goss, Jack A. MacAllister Chair in Regional Economics at Creighton University's Heider College of Business.

Jon Schmaderer, president of Tri-County Bank in Stuart, Nebraska said, “The calf market has now officially followed suit with grain and other livestock pricing declines.” Another bank CEO reported calf prices are going to be down 30 to 40 percent, which will have a large downward economic impact.

Bank CEOs project that more than one in five grain farmers, or 21.6 percent, will suffer negative cash flows for 2016. “This is 2.0 percent higher than the July 2016 projection when the same question was asked,” said Goss.

Farming and Ranching: The farmland and ranchland-price index for October fell to 25.0 from September’s 40.3. This is the 35th straight month the index has languished below growth neutral 50.0.

The October farm equipment-sales index sank to 13.1 from September’s 14.3. “Weakness in farm income and low agricultural commodity prices continue to restrain the sale of agriculture equipment across the region. This is having a significant and negative impact on both farm equipment dealers and agricultural equipment manufacturers across the region,” said Goss.

Banking: Borrowing by farmers remains strong as the October loan-volume index slipped to a strong 71.6 from last month’s 72.1. The checking-deposit index climbed to 63.7 from 50.0 in September, while the index for certificates of deposit and other savings instruments fell to 40.9 from 51.5 in September.

This month bankers were asked to identify the biggest challenge to their banking operations. More than one of four, or 27.3 percent, identified rising regulatory costs as their greatest challenge over the next five years. Almost one in 10, or 9.1 percent, reported farm foreclosures as the greatest economic challenge to their banking operations over a five-year time horizon.

Hiring: For the third time in the past four months, the Rural Mainstreet hiring index moved below growth neutral. The October hiring index declined to 45.4 from 54.8 for September. For the region, Rural Mainstreet employment is down by 1 percent over the past 12 months. Over the same period of time, urban employment for the region expanded by 1.5 percent.

Confidence: The confidence index, which reflects expectations for the economy six months out, was up slightly to 21.6 from September’s 21.5, indicating an intense pessimistic outlook among bankers. “Continuing weak grain and livestock commodity prices pushed banker’s economic outlook to October’s and September’s frail readings,” said Goss.

Home and Retail Sales: Home sales remain the positive indicator of the Rural Mainstreet economy with a 50.1 reading for October but down from September index of 57.2. The October retail-sales index increased to a very weak 36.3 from September’s 33.4. “Despite low inventories of homes for sale, Rural Mainstreet home sales continue on a positive trajectory, but rural retailers, much like their urban counterparts, are experiencing downturns in sales,” said Goss.

Each month, community bank presidents and CEOs in nonurban agriculturally and energy-dependent portions of a 10-state area are surveyed regarding current economic conditions in their communities and their projected economic outlooks six months down the road. Bankers from Colorado, Illinois, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, South Dakota and Wyoming are included. The survey is supported by a grant from Security State Bank in Ansley, Neb.

This survey represents an early snapshot of the economy of rural agriculturally and energy-dependent portions of the nation. The Rural Mainstreet Index (RMI) is a unique index covering 10 regional states, focusing on approximately 200 rural communities with an average population of 1,300. It gives the most current real-time analysis of the rural economy. Goss and Bill McQuillan, former chairman of the Independent Community Banks of America, created the monthly economic survey in 2005.

Farming and Ranching: The farmland and ranchland-price index for October fell to 25.0 from September’s 40.3. This is the 35th straight month the index has languished below growth neutral 50.0.

The October farm equipment-sales index sank to 13.1 from September’s 14.3. “Weakness in farm income and low agricultural commodity prices continue to restrain the sale of agriculture equipment across the region. This is having a significant and negative impact on both farm equipment dealers and agricultural equipment manufacturers across the region,” said Goss.

Banking: Borrowing by farmers remains strong as the October loan-volume index slipped to a strong 71.6 from last month’s 72.1. The checking-deposit index climbed to 63.7 from 50.0 in September, while the index for certificates of deposit and other savings instruments fell to 40.9 from 51.5 in September.

This month bankers were asked to identify the biggest challenge to their banking operations. More than one of four, or 27.3 percent, identified rising regulatory costs as their greatest challenge over the next five years. Almost one in 10, or 9.1 percent, reported farm foreclosures as the greatest economic challenge to their banking operations over a five-year time horizon.

Hiring: For the third time in the past four months, the Rural Mainstreet hiring index moved below growth neutral. The October hiring index declined to 45.4 from 54.8 for September. For the region, Rural Mainstreet employment is down by 1 percent over the past 12 months. Over the same period of time, urban employment for the region expanded by 1.5 percent.

Confidence: The confidence index, which reflects expectations for the economy six months out, was up slightly to 21.6 from September’s 21.5, indicating an intense pessimistic outlook among bankers. “Continuing weak grain and livestock commodity prices pushed banker’s economic outlook to October’s and September’s frail readings,” said Goss.

Home and Retail Sales: Home sales remain the positive indicator of the Rural Mainstreet economy with a 50.1 reading for October but down from September index of 57.2. The October retail-sales index increased to a very weak 36.3 from September’s 33.4. “Despite low inventories of homes for sale, Rural Mainstreet home sales continue on a positive trajectory, but rural retailers, much like their urban counterparts, are experiencing downturns in sales,” said Goss.

Each month, community bank presidents and CEOs in nonurban agriculturally and energy-dependent portions of a 10-state area are surveyed regarding current economic conditions in their communities and their projected economic outlooks six months down the road. Bankers from Colorado, Illinois, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, South Dakota and Wyoming are included. The survey is supported by a grant from Security State Bank in Ansley, Neb.

This survey represents an early snapshot of the economy of rural agriculturally and energy-dependent portions of the nation. The Rural Mainstreet Index (RMI) is a unique index covering 10 regional states, focusing on approximately 200 rural communities with an average population of 1,300. It gives the most current real-time analysis of the rural economy. Goss and Bill McQuillan, former chairman of the Independent Community Banks of America, created the monthly economic survey in 2005.

| Colorado: Colorado’s Rural Mainstreet Index (RMI) climbed to 68.5 from 54.7 in September. The farmland and ranchland-price index fell to 59.7 from September’s 69.7. Colorado’s hiring index for October sank to a solid 53.1 from September’s 73.2. Colorado job growth over the last 12 months; Rural Mainstreet, 2.5 percent; Urban Colorado, 2.8 percent. Illinois: The October RMI for Illinois slumped to 27.5 from 32.1 in September. The farmland-price index fell to 15.6 from September’s 26.3. The state’s new-hiring index sank to 42.8 from last month’s 50.7. Illinois job growth over the last 12 months; Rural Mainstreet, -2 percent; Urban Illinois 1 percent. Iowa: The October RMI for Iowa soared to 67.1 from September’s 56.2. Iowa’s farmland-price index for October increased to 47.8 from 47.2 in September. Iowa’s new-hiring index for October declined to a still strong 58.7 from September’s 65.1. Iowa job growth over the last 12 months; Rural Mainstreet, 2.4 percent; Urban Iowa, 1.1 percent. Kansas: The Kansas RMI for October slumped to 25.7 from September’s 35.4. The state’s farmland-price index for October tumbled to 18.9 from 24.2 in September. The new-hiring index for Kansas sank to 42.5 from 51.7 in September. Kansas job growth over the last 12 months; Rural Mainstreet, -2.9 percent; Urban Kansas, 0.5 percent. Minnesota: The October RMI for Minnesota tumbled to 26.3 from September’s 39.0. Minnesota’s farmland-price index fell to 23.8 from 26.3 in September. The new-hiring index for the state declined to 50.0 from last month’s 57.5. Minnesota job growth over the last 12 months; Rural Mainstreet, -0.4 percent; Urban Minnesota 1.8 percent. | Missouri: The October RMI for Missouri increased to 28.9 from September’s 26.4. The farmland-price index fell to 25.8 from September’s 29.7. Missouri’s new-hiring index plummeted to 18.7 from 35.6 in September. Missouri job growth over the last 12 months; Rural Mainstreet, -6.2 percent; Urban Missouri 1.8 percent. Nebraska: The Nebraska RMI for October sank to 51.1 from September’s 61.2. The state’s farmland-price index tumbled to 39.0 from September’s 46.9. Nebraska’s new-hiring index declined to 55.5 from 64.9 in September. Nebraska job growth over the last 12 months; Rural Mainstreet, 0.6 percent; Urban Nebraska, 1.2 percent. North Dakota: The North Dakota RMI for October slipped to 20.2 from 20.9 in September. The farmland-price index dipped to 18.2 from September’s 18.7. North Dakota’s new-hiring index plummeted to 19.2 from 37.8 in September. North Dakota job growth over the last 12 months; Rural Mainstreet, -7.1 percent; Urban North Dakota, 1.2 percent. South Dakota: The October RMI for South Dakota soared to 60.6 from September’s 52.1. The farmland-price index expanded to 42.3 from September’s 41.2. South Dakota's new-hiring index fell to 56.7 from September’s 62.8. South Dakota job growth over the last 12 months; Rural Mainstreet, 1.9 percent; Urban South Dakota, 3.4 percent. Wyoming: The October RMI for Wyoming slumped to 19.8 from 22.3 in September. The October farmland and ranchland-price index declined to 12.5 from September’s 19.7. Wyoming’s new-hiring index tumbled to 39.9 from September’s 48.5. Wyoming job growth over the last 12 months; Rural Mainstreet, -3 percent; Urban Wyoming, -2.6 percent. |

Tables 1 and 2 summarize the survey findings.

RSS Feed

RSS Feed