April 2023 Survey Results at a Glance:

- April’s overall reading, the Rural Mainstreet Index (RMI), rose above growth neutral for the month.

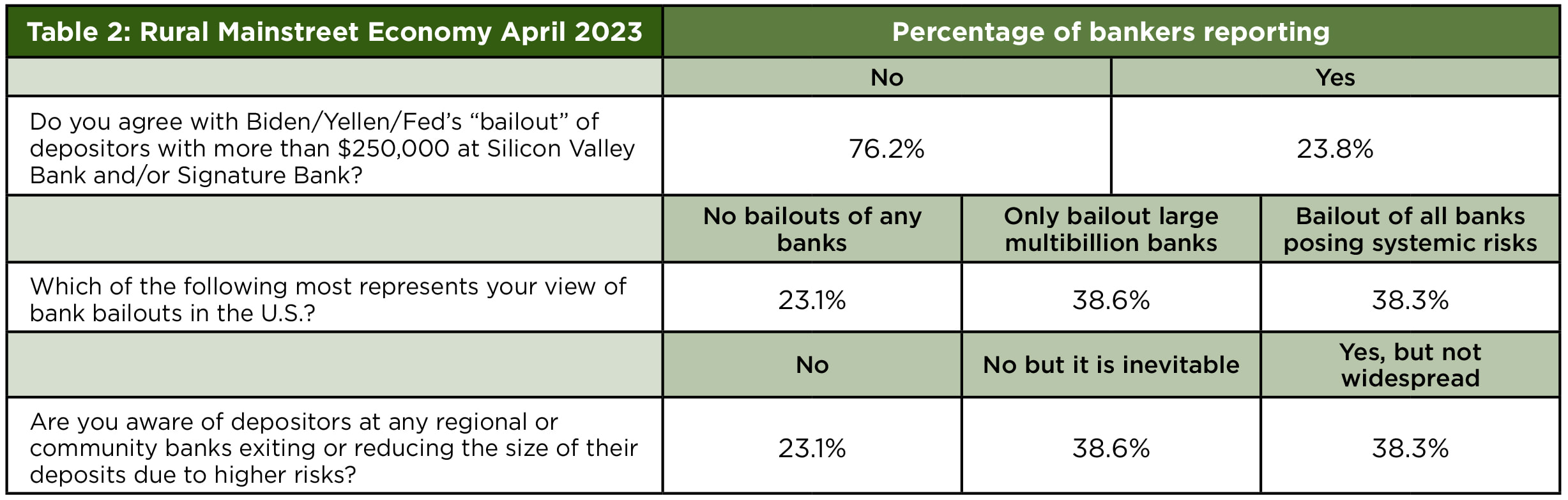

- More than three of four, or 76.2%, of bank CEOs oppose the recent “bailout” of Silicon Valley Bank and Signature Bank.

- Two-thirds of bank CEOs oppose all bank bailouts (i.e., community, regional and multibillion dollar banks).

- Approximately 64% of bankers reported depositors exiting due to higher financial risks.

- Checking deposits plummeted to a record low.

- Farmland prices expanded for the 31st straight month.

OMAHA, Neb. (April 20, 2023) -- After declining below growth neutral for March, the overall Rural Mainstreet Index expanded above the threshold for the month, according to the April monthly survey of bank CEOs in rural areas of a 10-state region dependent on agriculture and/or energy.

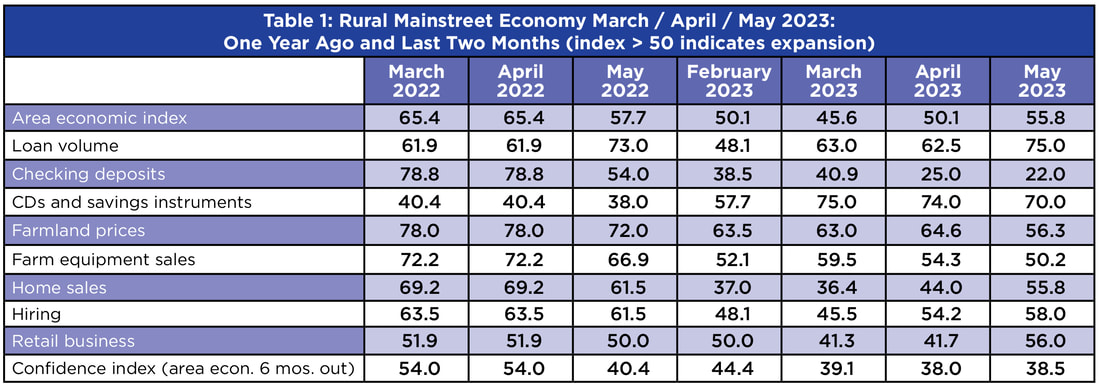

Overall: The region’s overall reading in April climbed to 50.1 from March’s 45.6. The index ranges between 0 and 100, with a reading of 50.0 representing growth neutral.

“The Rural Mainstreet economy continues to experience slow, to no, to negative economic growth. Only 8% of bankers reported improving economic conditions for the month with 84% indicating no change in economic conditions from March’s negative growth,” said Ernie Goss, PhD, Jack A. MacAllister Chair in Regional Economics at Creighton University’s Heider College of Business.

Overall: The region’s overall reading in April climbed to 50.1 from March’s 45.6. The index ranges between 0 and 100, with a reading of 50.0 representing growth neutral.

“The Rural Mainstreet economy continues to experience slow, to no, to negative economic growth. Only 8% of bankers reported improving economic conditions for the month with 84% indicating no change in economic conditions from March’s negative growth,” said Ernie Goss, PhD, Jack A. MacAllister Chair in Regional Economics at Creighton University’s Heider College of Business.

Mike Van Erdewyk, CEO of Breda Savings Bank in Breda, Iowa, said, “It seems like a self-fulfilling prophecy that they will say higher rates stopped inflation when it may be more of unprecedented government actions not letting the market sort it out.”

Farming and Ranching Land Prices: The region’s farmland price index rose to 64.6 from March’s 63.0. This was the 31st straight month that the index has advanced above 50.0.

Farm Equipment Sales: As a result of solid farm financial conditions, the farm equipment-sales index fell to a still solid 54.3 from 59.5 in March. The index has risen above growth neutral for 27 of the last 29 months.

Banking: The April loan volume index slipped to a still healthy 62.5 from 63.0 in March. The checking-deposit index plummeted to a record low 25.0 from March’s 40.9, while the index for certificates of deposit and other savings instruments dipped to 74.0 from March’s record high 75.0.

The record low checking deposit index is a real concern. According to Jeffrey Gerhart, former Chair of the Independent Community Bankers of America, “Depositors may move money around in order to keep under the $250,000 FDIC limit. This goes on frequently, so I don’t consider this a concern.”

Additionally, Gerhart advises depositors to visit with their bank about the various options available to reduce depositor risks.

Bank CEOs were asked several questions regarding the recent bank failures of Silicon Valley Bank and Signature Bank:

Farming and Ranching Land Prices: The region’s farmland price index rose to 64.6 from March’s 63.0. This was the 31st straight month that the index has advanced above 50.0.

Farm Equipment Sales: As a result of solid farm financial conditions, the farm equipment-sales index fell to a still solid 54.3 from 59.5 in March. The index has risen above growth neutral for 27 of the last 29 months.

Banking: The April loan volume index slipped to a still healthy 62.5 from 63.0 in March. The checking-deposit index plummeted to a record low 25.0 from March’s 40.9, while the index for certificates of deposit and other savings instruments dipped to 74.0 from March’s record high 75.0.

The record low checking deposit index is a real concern. According to Jeffrey Gerhart, former Chair of the Independent Community Bankers of America, “Depositors may move money around in order to keep under the $250,000 FDIC limit. This goes on frequently, so I don’t consider this a concern.”

Additionally, Gerhart advises depositors to visit with their bank about the various options available to reduce depositor risks.

Bank CEOs were asked several questions regarding the recent bank failures of Silicon Valley Bank and Signature Bank:

- More than three of four, or 76.2%, of bank CEOs oppose the recent Biden/Yellen/Fed bank bailout of Silicon Valley Bank and Signature Bank.

- Two-thirds of bank CEOs oppose all bank bailouts (i.e., community, regional and multibillion dollar banks).

- Approximately 29.1% support bailouts of all banks posing systemic risks.

- Approximately 64% reported depositors exiting due to higher financial risks.

Larry Winum, CEO of Glenwood State Bank in Glenwood Iowa, said, “How many times is our government going to bail out banks and make all banks pay for it through increased FDIC premiums and assessments?”

Winum argues that the FDIC should listen to community banks and establish “risk based” premium fee structures. “The current methodology punishes community banks,” said Winum.

Jeff Bonnett, CEO of Havana National Bank in Havana, Ill., said, “Although I am a firm believer in capitalism and all the positive and negative consequences (bank/business failures) that go with such an economic system, I do believe that the FDIC and the banking industry needs to evaluate and make changes to the current system of deposit insurance.”

Bonnett argues that large corporate and organizational deposit accounts such as payroll and operating accounts need a separate format of FDIC insurance.

Hiring: The new hiring index for April climbed to 54.2 from 45.5 in March. Labor shortages continue to be a significant issue constraining growth for Rural Mainstreet businesses. Over the past 12 months, the Rural Mainstreet Economy has expanded jobs by 2.8% compared to a lower 2.1% for urban areas of the same 10 states.

Confidence: The slowing economy, higher borrowing costs and labor shortages continued to constrain the business confidence index to a weak 38.0, down from March’s 39.1. “Over the past 12 months, the regional confidence index has fallen to levels indicating a very negative outlook,” said Goss.

Home and Retail Sales: Home-sales climbed to 44.0 from March’s 36.4. “This is the eleventh straight month that the home-sales index has fallen below growth neutral. A slowing economy, higher mortgage rates and low housing inventories for the past year slowed home sales in the region over that time period,” said Goss.

The retail-sales index for April increased slightly to a weak 41.7 from March’s 41.3. “Bankers were pessimistic regarding the economic outlook for retail sales for the second quarter after an anemic quarter one,” said Goss.

Winum argues that the FDIC should listen to community banks and establish “risk based” premium fee structures. “The current methodology punishes community banks,” said Winum.

Jeff Bonnett, CEO of Havana National Bank in Havana, Ill., said, “Although I am a firm believer in capitalism and all the positive and negative consequences (bank/business failures) that go with such an economic system, I do believe that the FDIC and the banking industry needs to evaluate and make changes to the current system of deposit insurance.”

Bonnett argues that large corporate and organizational deposit accounts such as payroll and operating accounts need a separate format of FDIC insurance.

Hiring: The new hiring index for April climbed to 54.2 from 45.5 in March. Labor shortages continue to be a significant issue constraining growth for Rural Mainstreet businesses. Over the past 12 months, the Rural Mainstreet Economy has expanded jobs by 2.8% compared to a lower 2.1% for urban areas of the same 10 states.

Confidence: The slowing economy, higher borrowing costs and labor shortages continued to constrain the business confidence index to a weak 38.0, down from March’s 39.1. “Over the past 12 months, the regional confidence index has fallen to levels indicating a very negative outlook,” said Goss.

Home and Retail Sales: Home-sales climbed to 44.0 from March’s 36.4. “This is the eleventh straight month that the home-sales index has fallen below growth neutral. A slowing economy, higher mortgage rates and low housing inventories for the past year slowed home sales in the region over that time period,” said Goss.

The retail-sales index for April increased slightly to a weak 41.7 from March’s 41.3. “Bankers were pessimistic regarding the economic outlook for retail sales for the second quarter after an anemic quarter one,” said Goss.

The survey represents an early snapshot of the economy of rural agriculturally and energy-dependent portions of the nation. The Rural Mainstreet Index is a unique index covering 10 regional states, focusing on approximately 200 rural communities with an average population of 1,300. The index provides the most current real-time analysis of the rural economy. Goss and Bill McQuillan, former Chairman of the Independent Community Banks of America, created the monthly economic survey and launched it in January 2006. Below are the state reports:

| Colorado: Colorado’s RMI for April rose to 53.1 from March’s 50.3. The farmland- and ranchland-price index for April advanced to 65.6 from 64.3 in March. The state’s new hiring index was 54.9, up from 47.8 for March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 4.5% compared to 1.4% for urban areas of the state. Illinois: The April RMI for Illinois increased to 49.6 from March’s 42.0. The farmland-price index climbed to 61.9 from 60.8 in March. The state’s new-hiring index rose to a tepid 50.5 from March’s 43.5. Jim Eckert, CEO of Anchor State Bank in Anchor, reported that, “We're just going into planting mode. Moisture levels are adequate, but not optimal.” Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 3.3% compared to 2.2% for urban areas of the state. Iowa: Iowa’s April RMI slumped to 44.8 from 46.7 in March. Iowa’s farmland-price index increased to 57.4 from March’s 55.6. Iowa’s new-hiring index for April moved higher to 44.8 from 37.1 in March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 0.7% compared to 2.0% for urban areas of the state. Kansas: The Kansas RMI for April climbed to 52.1 from March’s 43.6. The state’s farmland-price index increased to 63.3 from 61.4 in March. The April new-hiring index for Kansas rose to 52.1 from 44.3 in March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 4.0% compared to 2.7% for urban areas of the state. Minnesota: The April RMI for Minnesota increased to 50.9 from March’s 42.0. Minnesota’s farmland-price index climbed to 62.8 from 61.5 in March. The new-hiring index for April climbed to 54.7 from 44.4 in March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 3.4% compared to 2.0% for urban areas of the state. | Missouri: The state’s April RMI dropped to 41.3 from 44.5 in March. The farmland-price index fell to 60.6 from March’s 61.8. The state’s new hiring gauge rose to 53.2 from 44.8 in March. Over the past 12 months, the state’s Rural Mainstreet Economy experienced job losses of 0.2% compared to a gain of 2.4% for urban areas of the state. Nebraska: The Nebraska RMI climbed above growth neutral to 52.7 from 48.3 in March. The state’s farmland-price index for April rose to 65.4 from March’s 63.4. Nebraska’s April new-hiring index grew to 57.8 from 46.8 in March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 4.8% compared to 1.2% for urban areas of the state. North Dakota: North Dakota’s RMI for April soared to 55.7 from March’s 39.0. The state’s farmland-price index expanded to 61.4 from 59.5 in March. The state’s new-hiring index climbed to 57.8 from 41.9 in March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 3.5% compared to 2.5% for urban areas of the state. South Dakota: The April RMI for South Dakota slumped to 39.5 from 47.2 in March. The state’s farmland-price index increased to 59.8 from March’s 58.8. South Dakota’s April new hiring index expanded to 47.8 from 41.0 in March. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 1.2% compared to 3.4% for urban areas of the state. Wyoming: The April RMI for Wyoming grew to 44.5 from 41.7 in March. The April farmland- and ranchland-price index increased to 61.9 from 60.6 in March. Wyoming’s new-hiring index expanded to 50.5 from March’s 43.3. Over the past 12 months, the state’s Rural Mainstreet Economy expanded jobs by 2.7% compared to 2.3% for urban areas of the state. |

Tables 1 and 2 summarize the survey findings. (Click each table to view larger.)

RSS Feed

RSS Feed